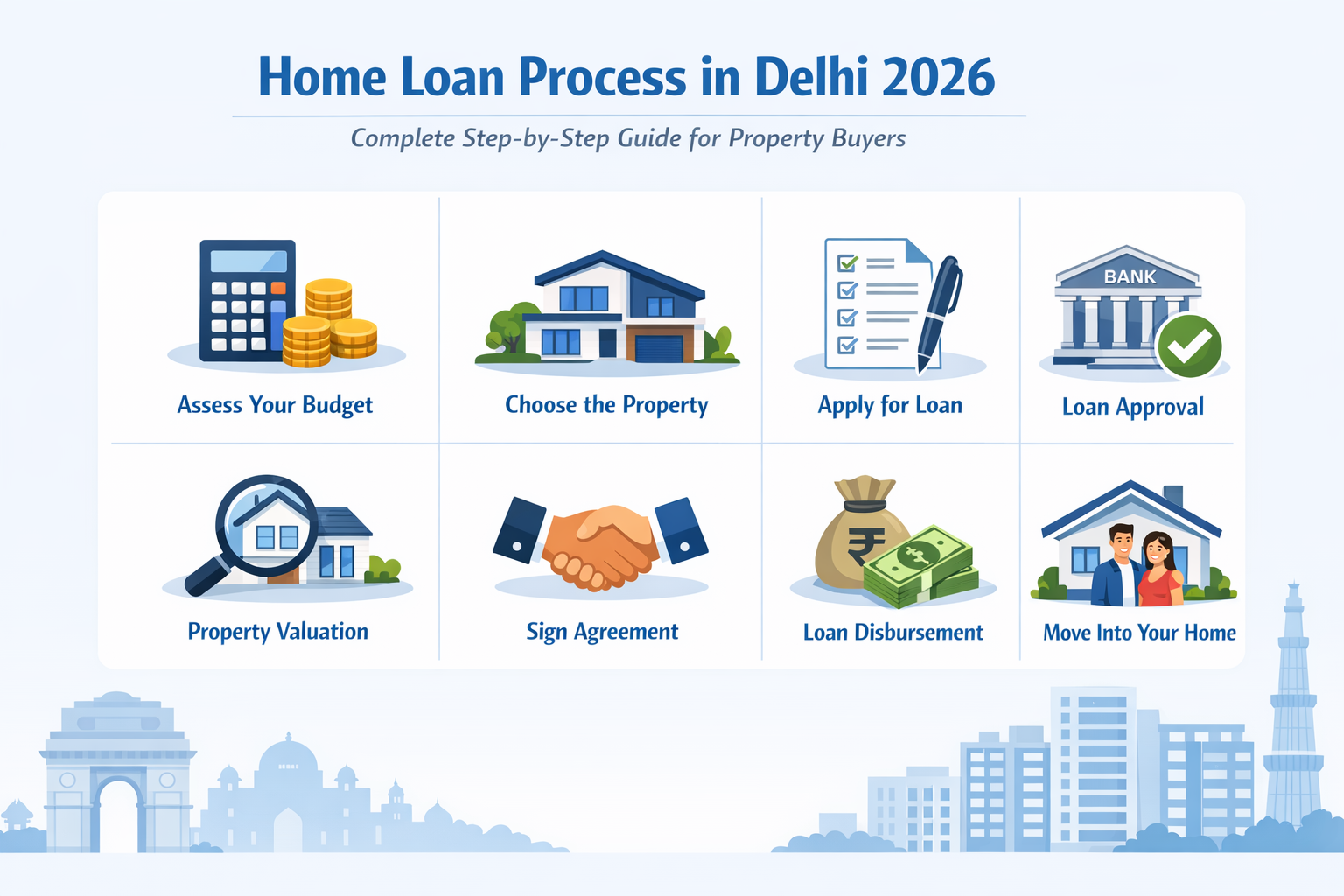

Understanding the Home Loan Process in Delhi 2026 is crucial if you are planning to buy property this year. Whether you are purchasing a flat, builder floor, DDA property, or resale home, knowing how the Home Loan Process in Delhi 2026 works can save you time, money, and rejection stress.

Many buyers lose property deals because they are unaware of documentation requirements or approval timelines. This detailed guide explains everything about the Home Loan Process in Delhi 2026, including eligibility, interest rates, approval stages, disbursement, and common mistakes to avoid.

What Is the Home Loan Process in Delhi 2026?

The Home Loan Process in Delhi 2026 is the procedure through which banks and housing finance companies evaluate your financial profile and approve funding for property purchase.

It typically involves:

-

Loan application

-

Document submission

-

Credit score check

-

Property verification

-

Loan approval

-

Disbursement

Step 1: Check Eligibility Before Applying

Before starting the Home Loan Process in Delhi 2026, check if you meet basic eligibility criteria:

Age

21 to 65 years

Employment Type

-

Salaried employees

-

Self-employed professionals

-

Business owners

Minimum Income

Depends on bank and property value.

CIBIL Score

Minimum 700+ recommended for smooth approval.

A strong profile improves your chances during the Home Loan Process in Delhi 2026.

Step 2: Decide Loan Amount and EMI Capacity

Banks generally finance:

-

Up to 75%–90% of property value

-

Remaining amount must be paid by buyer (down payment)

Before entering the Home Loan Process in Delhi 2026, calculate:

-

Monthly EMI affordability

-

Other ongoing loans

-

Financial stability

Financial discipline increases approval chances.

Step 3: Choose the Right Bank or Lender

In Delhi, major banks offering home loans include:

-

State Bank of India

-

HDFC Bank

-

ICICI Bank

-

Axis Bank

-

Punjab National Bank

Compare:

-

Interest rates

-

Processing fees

-

Prepayment charges

-

Floating vs fixed rate

Choosing the right lender simplifies the Home Loan Process in Delhi 2026.

Step 4: Documents Required for Home Loan Process in Delhi 2026

Proper documentation is critical.

Identity Proof

-

Aadhaar Card

-

PAN Card

Address Proof

-

Utility bill

-

Passport

Income Proof (Salaried)

-

Last 3 months salary slips

-

6 months bank statement

-

Form 16

Income Proof (Self-Employed)

-

ITR (2–3 years)

-

Balance sheet

-

Business proof

Property Documents

-

Sale agreement

-

Chain documents

-

Approved building plan

-

NOC (if applicable)

Incomplete documents delay the Home Loan Process in Delhi 2026.

Step 5: Property Legal and Technical Verification

Banks conduct:

-

Legal verification (ownership clarity)

-

Technical valuation (market value check)

-

Circle rate comparison

If property has legal issues, the Home Loan Process in Delhi 2026 may be rejected.

Step 6: Loan Sanction Letter

Once verified, the bank issues a sanction letter mentioning:

-

Loan amount

-

Interest rate

-

EMI

-

Tenure

-

Conditions

This is conditional approval in the Home Loan Process in Delhi 2026.

Step 7: Loan Agreement Signing

You must sign:

-

Loan agreement

-

ECS/NACH mandate

-

Disbursement request

After this, the Home Loan Process in Delhi 2026 moves to final stage.

Step 8: Loan Disbursement

Disbursement may be:

-

Full (for resale property)

-

Stage-wise (for under-construction property)

Funds are directly transferred to seller or builder.

Interest Rates in Home Loan Process in Delhi 2026

Interest rates depend on:

-

Credit score

-

Income stability

-

Employment type

-

Bank policies

Floating rates are more common in 2026.

Processing Fees in Delhi 2026

Typical charges:

-

0.25% to 1% of loan amount

-

Plus GST

Some banks offer festive waivers.

Common Reasons for Home Loan Rejection

During the Home Loan Process in Delhi 2026, rejection may happen due to:

❌ Low CIBIL score

❌ High existing loans

❌ Property legal issues

❌ Income mismatch

❌ Fake documents

Proper preparation prevents rejection.

Tips to Get Faster Approval in 2026

✔ Maintain 750+ credit score

✔ Keep debt-to-income ratio low

✔ Submit accurate documents

✔ Choose pre-approved projects

✔ Avoid multiple loan applications

These improve the success rate of the Home Loan Process in Delhi 2026.

Timeline of Home Loan Process in Delhi 2026

| Stage | Time Required |

|---|---|

| Application Review | 2–3 days |

| Credit Check | 1–2 days |

| Property Verification | 3–7 days |

| Sanction Letter | 7–10 days |

| Disbursement | 2–5 days |

Total: 10–20 days average.

Tax Benefits in 2026

Under Income Tax rules:

-

₹2 lakh deduction on interest

-

₹1.5 lakh deduction on principal

-

Additional benefits for first-time buyers (if applicable)

Tax savings make the Home Loan Process in Delhi 2026 financially beneficial.